Given the growing popularity of equity compensation plans amongst the country’s largest corporations, offering stock to employees has become a crucial employee benefit. One of the most common forms of equity compensation are known as Restricted Stock Units, or RSUs for short.

According to a 2020 survey from Charles Schwab, 5 in 10 millennials said that equity compensation was one of the main reasons why they took their job. Clearly, equity compensation is playing an increasingly important role in attracting and retaining talent in today’s labor market.

Offering stock to employees can create a win-win scenario, especially in an environment of increasing stock prices. Companies can control cash flow and align incentives, while employees benefit from increased pay. However, this assumes the stock price continues to rise. Once the stock price falls, even by a little bit, these incentives can become disincentives. At this point, employees start to reevaluate if it’s worth holding onto their shares.

There are many articles and videos on the internet that do a good job explaining what RSUs are, how vesting schedules work, the difference between RSUs and stock options, the tax treatment, etc. Here are two good links discussing the basics: Investopedia and Millennial Wealth

We frequently get the following questions from clients about their RSUs:

- “I want to (buy a house/pay for my kids’ school/buy a new car/etc.), but need to save for the future, what should I do with these shares?”

- “The stock has gone up (or down) a ton! Should I sell or should I hold?”

- “I’m planning on getting a new job soon, what should I do with these?”

- “I have no idea what these things are, can you help me with it?”

You’re not alone, these are extremely common questions that require thoughtful consideration about your financial situation, objectives, and views on risk. Like most things in personal finance, there’s not a “one-size-fits-all” solution. That’s why they call it personal finance, it’s personal!

Your best bet is to come up with a plan before you have to make a decision, because in the moment, it’s easy to become emotional and swayed by recent events. Obviously, everyone’s situation is different, so when working with clients who receive equity compensation, we like to ask them a series of questions to help them gather their thoughts around what they should do.

Here are the main question we like to ask:

If you were given a cash bonus, what would you do with it? would you treat yourself? would you save it? would you pay down debt? would you invest it? would you buy your company stock?

Believe it or not, receiving RSUs and a cash bonus are basically the same thing – when RSUs vest, it’s as if you were to take a cash bonus and invest 100% of it directly into your company stock! The tax treatment is exactly the same. They are both taxed as ordinary income (at the RSU vest date). RSUs are just another form of compensation, the same as receiving an increased salary, although its exact value is unknown until the shares vest.

We like to ask this question to clients to help them understand this relationship and unpack their feelings towards the stock. When given cash bonuses, most people spend and save a portion of it. If that’s the case, the decision as to what to do with your RSUs should be no different. Treat them as cash and sell the shares as they vest to meet your life’s needs.

Typically, the default option at most companies for handling your RSUs at the vest date is to do nothing – meaning once the shares vest, you now own those shares. But, going back to our question above, this is essentially the same thing as you receiving a cash bonus and immediately buying shares in your company. Is this your intention? If it is, great keep on doing what you’re doing. If you’re unsure, here are some other questions to ask yourself.

Four other questions to consider:

1. What’s the time horizon for my financial goals? In how many years do you want to purchase [insert whatever pops into your mind]? Am I viewing these shares as a part of funding this goal, or are they for something else?

An important consideration for any financial goal is time horizon, and naturally, the time horizon of your goal impacts your willingness to stomach volatile stock prices and take on risk. It’s important to ask yourself, is the upside worth the downside risk, especially if you have a short-term financial goal coming up. Stock prices can change quickly, just look at the next question.

It’s important to mention that holding or selling your shares isn’t a zero-sum game. When introducing the concept of selling your RSUs, a handful of people will immediately think about the huge opportunity that they’ve just lost out on by selling, especially when their company’s stock inevitably “goes to the moon!” However, what many fail to consider is that you can always use the proceeds from selling your RSUs and invest it in a diversified portfolio. Not to mention, if you have unvested shares coming your way, you’ll still benefit from an increasing stock price as a part of your ONGOING compensation!

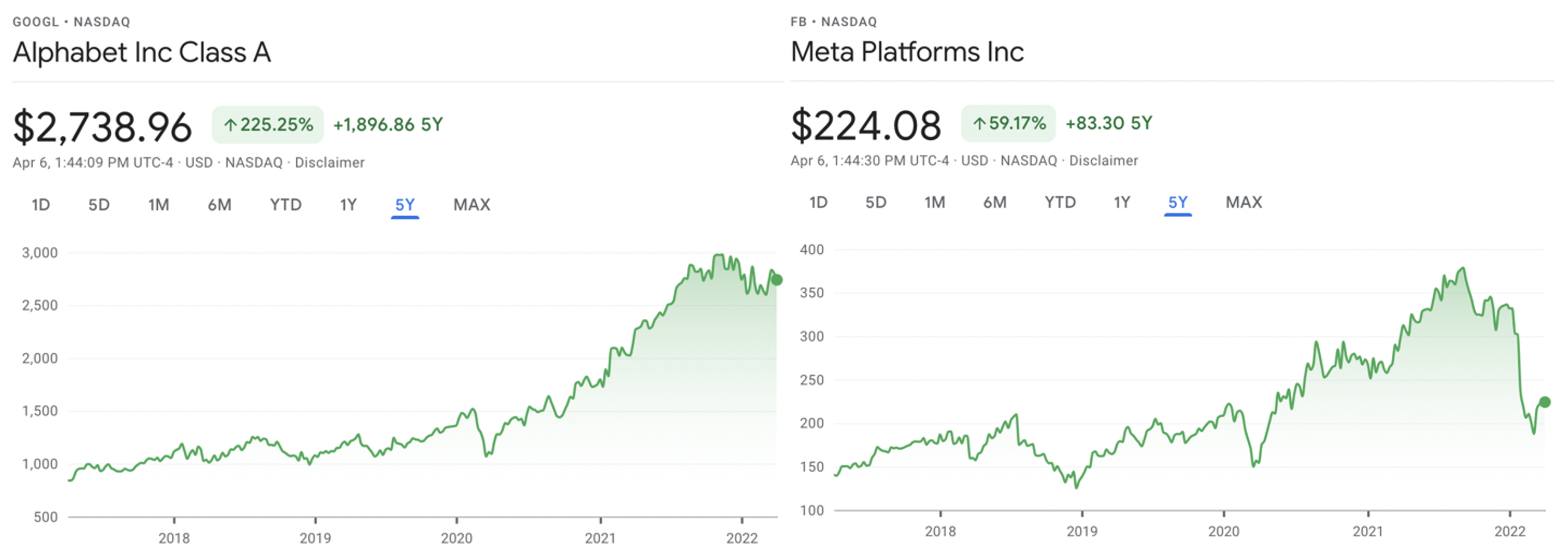

2. What would feel worse, holding onto your shares and the stock immediately falls by 20%, or selling your shares and the stock immediately rises by 20%?

Both situations are not ideal, but both are within the realm of possibilities. Really what we’re getting at here is regret minimization. Here are some familiar companies where a similar situation has happened.

Stock prices of Alphabet (Google) and Meta Platforms (Facebook) over the last 5 years. [As of 4/6/22]

3. How do you view your company and the trajectory it’s on? If you didn’t work there, how much of the stock would you be willing to purchase?

It’s human nature to have biases! If you’re working for the company, you probably believe in what the company stands for and where it’s headed. Being an employee, you naturally have greater insight into the company’s inner workings and potential. At the same time, this could create some blind spots.

It’s important to consider that you’re not only “concentrated” in the shares you own, but you also receive your paycheck from the exact same entity. Here are some examples of news articles that highlight this risk: General Electric, Zillow, Peloton, Expedia.

4. Imagine you’re retired, at what percentage of your life savings would you feel comfortable holding in a single company? 10%, 20%, 50%?

When you retire, you’ll likely have a fraction of the income you’ve had during your working years (don’t forget about Social Security). At some point, you’re probably going to have to sell some of your investments. At the end of the day, that’s why most people invest, to grow your money to be able to spend much more of it and ENJOY it at a future date.

If you’re hesitant to sell some along the way, a good chunk of your assets might be tied up in the company by the time you retire. Don’t get me wrong, this could be a great situation, but you could also have too many eggs in one basket with a large tax bill. This could cause some headaches down the road.

It’s important to figure out what feels comfortable for you and recognize that this will likely change over your life. Concentration builds wealth, diversification protects it.

If it isn’t clear by now, the most effective thing you can do is to come up with a plan. The most optimal plan is a plan that you’re going to stick with no matter what happens to the stock price. If you need guidance in figuring out what that plan is, we’re more than happy to help!