Each year the Social Security Administration releases their Annual Trustees Report, which provides information about the projected funding levels of the Social Security trust fund. Unless you’re looking for great bedside reading material, you probably haven’t read this year’s report. Here’s the TLDR version – the Social Security trust fund will run out of money by 2033.

Society has accepted many things as common knowledge, like swallowed bubble gum taking seven years to digest or angry bulls charging when they see red. We’ve spent most of our lives believing these myths to be true and haven’t been told otherwise. In the same way, many have accepted that younger generations will not receive Social Security, or that Congress is plundering our Social Security funds for other government spending. We’ll debunk these common myths below.

If you were wondering, gum passes through your digestive system in about seven days and bulls are color blind.

As it stands today, if the Social Security trust fund were to run out of money it would still be able to pay 76% of scheduled benefits. 1 How does this make sense if the trust funds run out of money? Essentially, the government would be spending its entire paycheck. In other words, each year’s Social Security taxes received from the work force would be used to pay for that year’s benefits. In this worst-case scenario, benefits would be cut, but at least Social Security recipients are not left with merely a participation trophy.

Now this would be a catastrophic scenario, but not all hope is lost. The good news is Congress has multiple levers that can be pulled to ensure the Social Security Administration can fully pay benefits and maintain solvency through 2033 and beyond.

How important is Social Security?

Established in the aftermath of the Great Depression, Social Security was designed to create a social safety net for America’s elderly. Today, Social Security benefits provide a source of income for an average of 65 million people per month and is expected to pay over one trillion dollars in benefits to the elderly, disabled, and survivor population just this year. 2 For this post, we define “elderly” as those who are 65 years and older, however, you can claim Social Security benefits as early as 62 years old.

Here are some facts that show why Social Security is important to so many Americans: 2

- Nearly 9 out of every 10 people who are elderly, receive Social Security benefits

- Social Security benefits represent about 30% of the income of the elderly

- Among the elderly, nearly 4 out of every 10 beneficiaries receive 50% or more of their income from Social Security and about 1 out of every 10 beneficiaries receive 90% or more of their income from Social Security

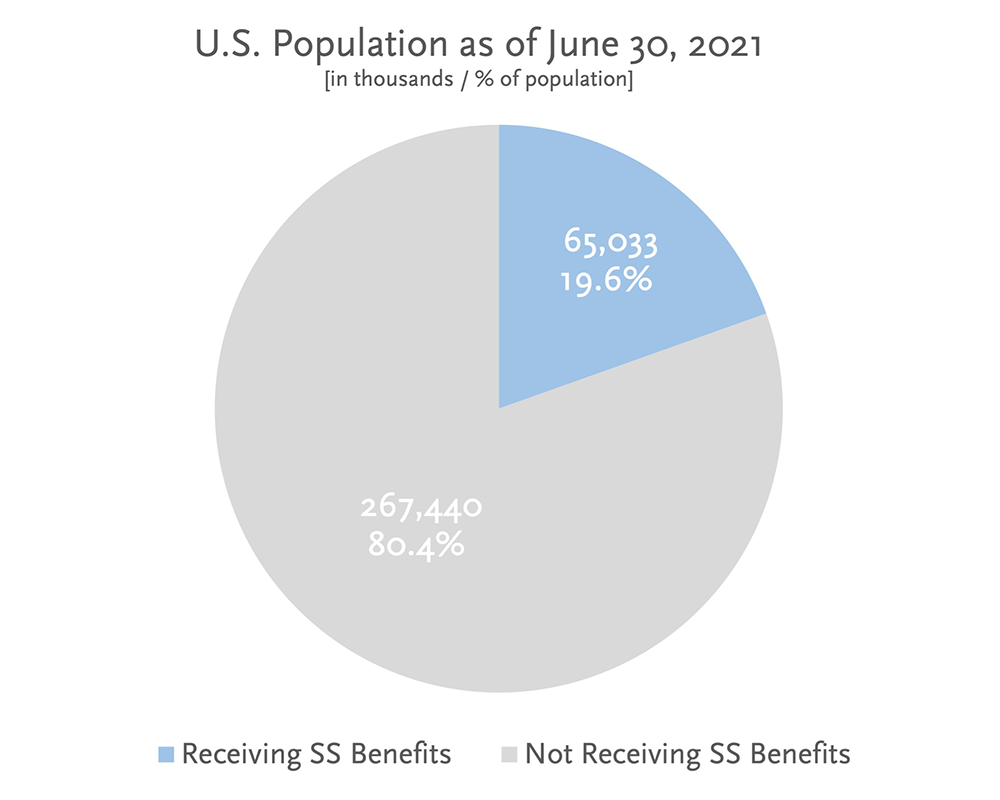

U.S. population broken out by those receiving Social Security benefits and those who are not:

As of June 30, 2021, nearly 20% of Americans received Social Security. 3

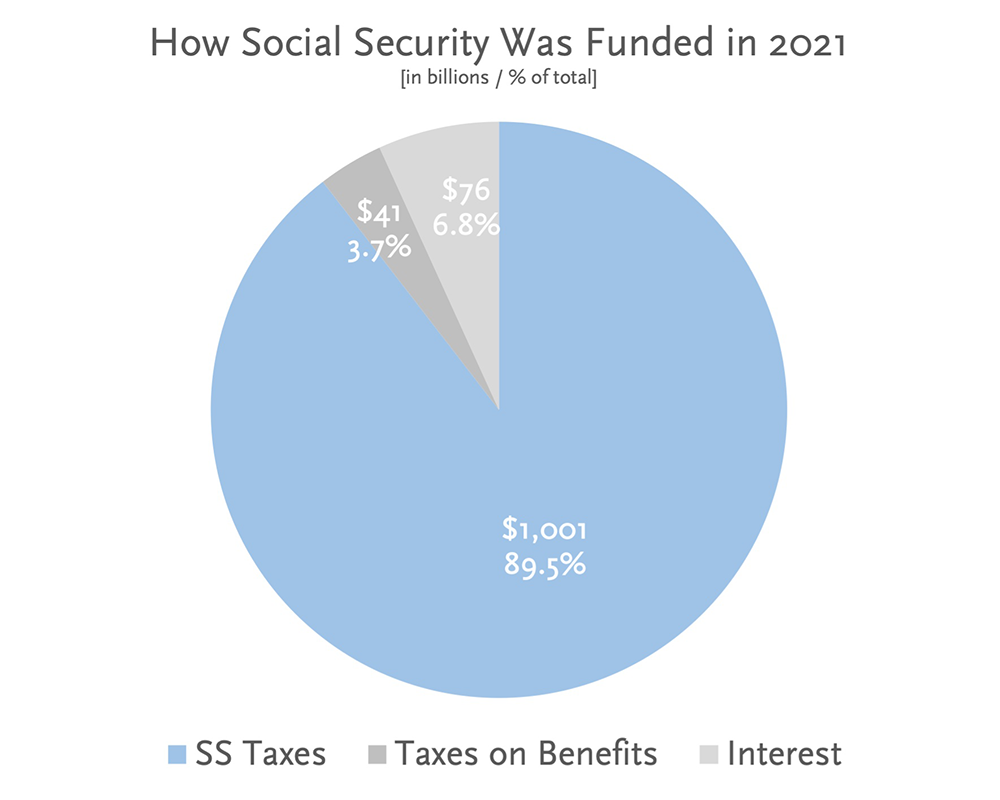

How we pay for Social Security:

Nearly 90% of Social Security funding comes from payroll taxes. 4

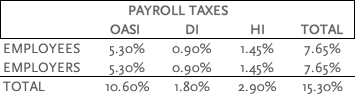

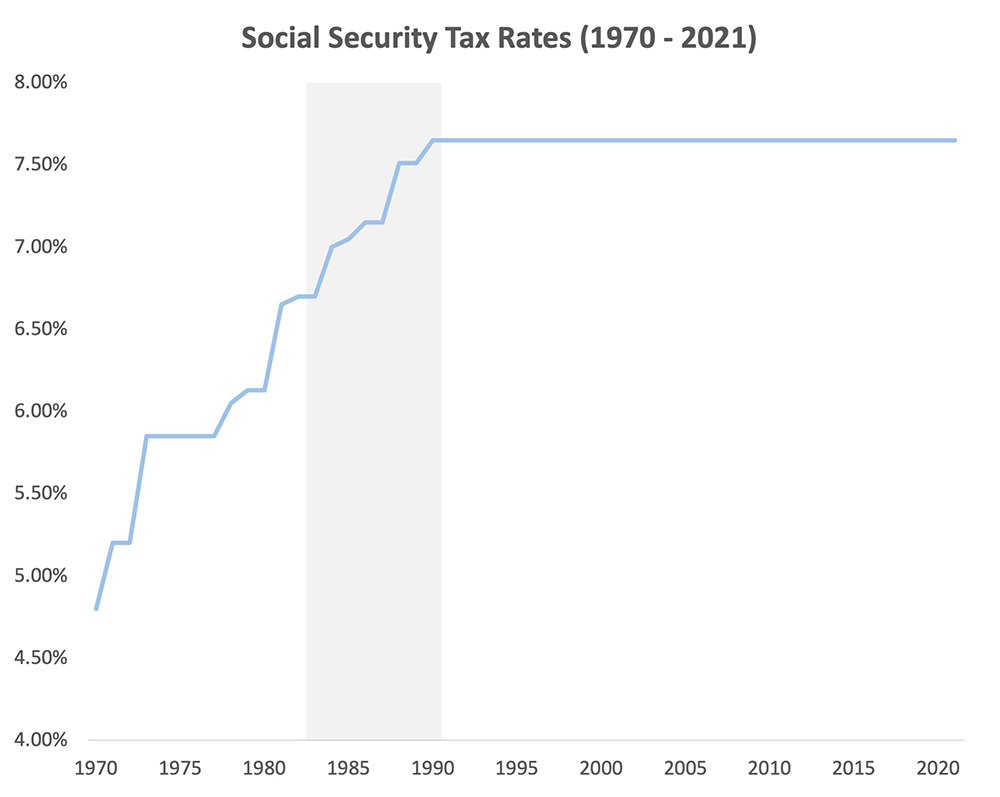

Social Security tax rates deducted from the average paycheck:

Our payroll taxes fund three different trust funds: the Old-Age and Survivors Insurance fund (OASI), the Disability Insurance fund (DI), and Hospital Insurance fund (HI – also known as Medicare). For the blog, we’ll focus on the OASI fund, which is the fund that pays retirement and survivor benefits.

Why is the Social Security trust fund running out of money?

Simply put, there are more retired people taking Social Security benefits and not enough working people to replenish the funds used to pay for those benefits. This is due to a significant demographic shift, caused by a variety of factors including: changes in birth rates, longer life expectancies, improved healthcare, cost of living factors, etc. As an example, when Social Security was created in 1935, the average life expectancy was 61 for men and 65 for women. Today, the pre-pandemic number is closer to 76 and 81, respectively.5

To be sure, Congress has not raided the Social Security trust fund. Technically speaking, Congress does borrow from Social Security due to its investments in US Treasuries, but that is the extent of it. As with all US Treasury debt obligations, the government is obligated to pay it back with interest. The truth is, Congress has not used the trust funds for anything other than its intended purpose. Here’s a LINK to some other myths that the Social Security Administration has debunked.

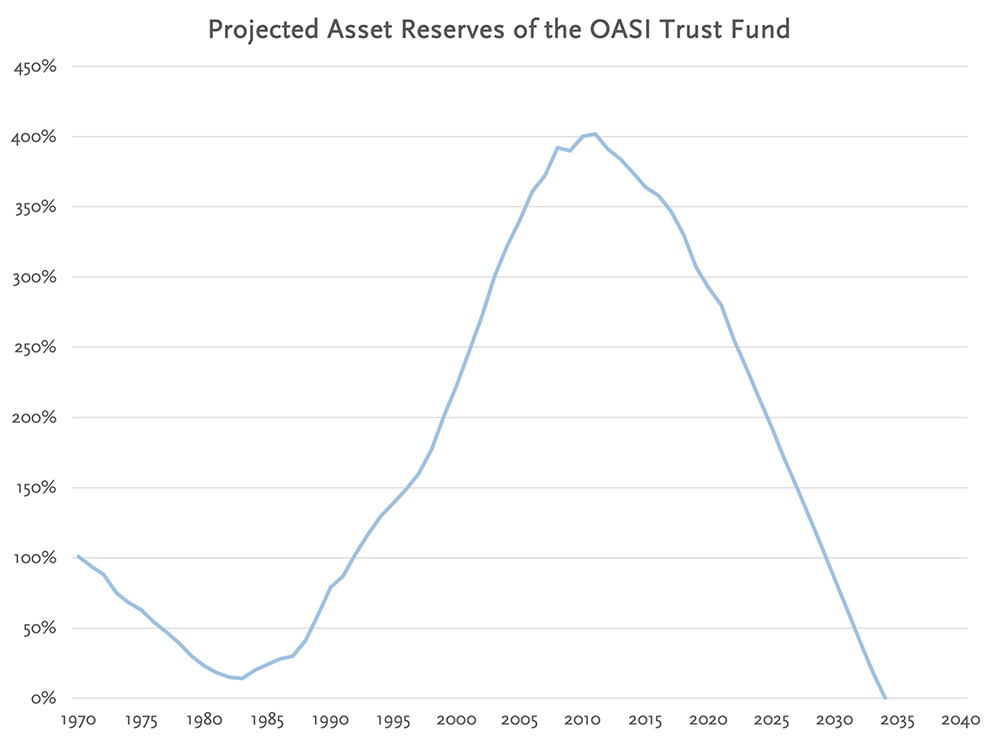

So, how are we looking today? Let’s look at the line chart below which shows the past, current, and projected asset reserve funding ratios of the OASI trust fund. As a reminder, the OASI trust fund is the fund that pays retirement and survivor benefits.

At the end of 2020, the trust fund is 292% funded, but we can see a sharp decline all the way down to 0% in 2033. In 1983, the OASI trust fund was only 14% funded. 1

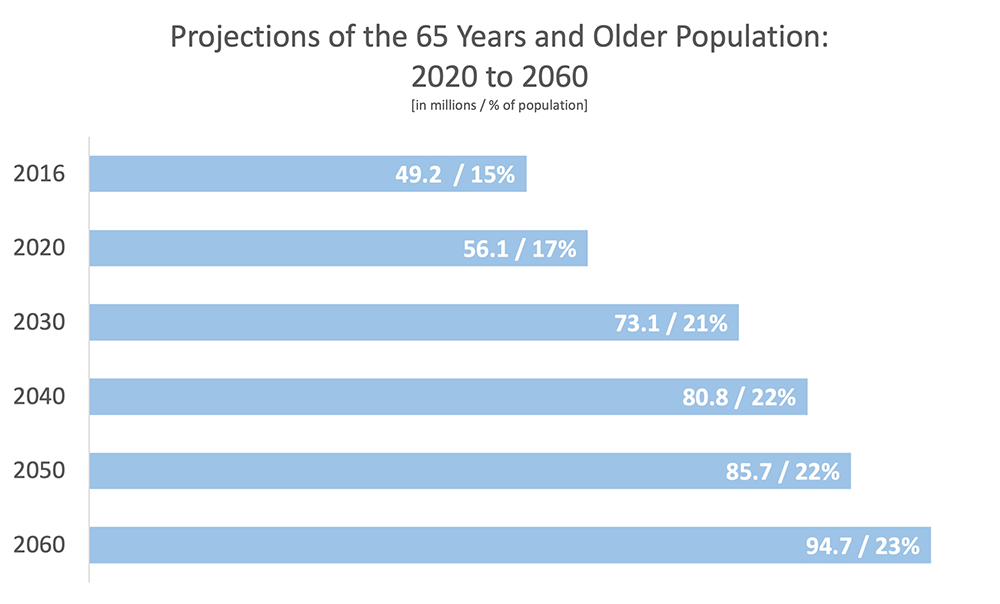

Why is there such a steep decline? Let’s look at the next chart from the US Census Bureau which shows us population projections for the elderly over the next 40 years.

Currently, in the US, there are roughly 56 million elderly people, representing 17% of the population. By 2030 there are projected to be 73 million elderly people, or 21% of the population. By 2060, the elderly will represent nearly 23% of the population. 6

America is aging very quickly. According to demographic projections by the US Census Bureau, in the year 2034, it is projected that the elderly will outnumber children for the first time in U.S. history. 6

We’ve seen this before.

In the early 80’s, the Social Security trust fund was projected to only be months away from running out of money before Congress stepped in… talk about a buzzer beater. Under the Reagan administration, the 1983 Amendments were passed, which alleviated the short-term financing pressures the fund was under. The primary provisions of the act involved:

- Taxing Social Security benefits (Yes, you can get taxed on Social Security)

- Increasing the full retirement age

- Accelerating already scheduled increases in tax rates

Why is this important? It is important because it means we’re not in uncharted waters. There is precedent to protect Social Security benefits through bi-partisan legislation, highlighting that both political parties have a vested interest.

Below is a line chart showing the changes in Social Security tax rates from the 70’s through the 80’s. The shaded area in the line chart represents the period immediately after the ‘83 Amendments. You can see that tax rates have been flat ever since. 7

What can we do now?

The Social Security trust fund has been projected to be depleted in the 2030’s for over a decade. As a result, a lot of smart people have researched potential solutions. Some of the most popular solutions to resolving the shortfall include the following:

- Increasing the earnings cap on Social Security taxes which is currently set at $147,000 beginning in 2022

- Increasing taxes that fund the OASI/DI trust funds from the current 12.4% to 15.76% today, or 16.6% in 2034

- Reducing cost of living adjustments (these adjust yearly to keep up with inflation)

- Gradually increasing the full retirement age from 67 to 70

It’s also worth noting that these proposed solutions are not mutually exclusive of each other. If you’re interested on possible solutions or have trouble sleeping, click HERE for additional reading.

Like anything in life, there will be trade-offs. Since we don’t have a crystal ball, the future of Social Security benefits will be uncertain. However, at the very least, we can take some comfort in knowing that Social Security will likely continue to exist and will be paid for, in some fashion, well past 2033.

Blog References

- Social Security 2021 Annual Trustees Report

- Social Security Administration Fact Sheet: June 2021

- United States Census Bureau Population Clock: June 2021

- Summary: Actuarial Status of the Social Security Trust Funds: August 2021

- CDC: Mortality Trends in the United States, 1900 -2018

- Demographic Turning Points for the United States: Population Projections for 2020 to 2060

- Social Security Administration: Social Security and Medicare Tax Rates

- Social Security Administration: Contribution and Benefit Base