LOOKING BACK

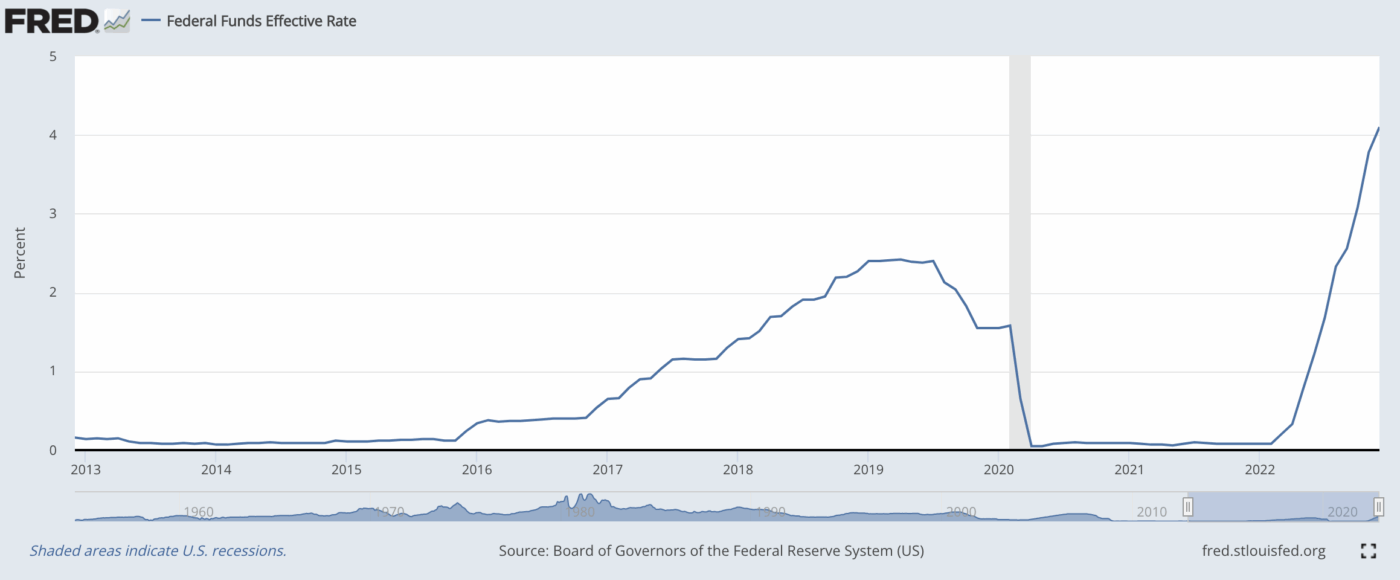

It’s difficult to know what the future will hold without understanding the past. 2022 was a difficult year in the market. An unprecedented, rapid increase in interest rates by the Federal Reserve, created significant market volatility and negative returns for the year:

Consequently, the S&P 500 finished down -19.44% and investors experienced the risk side of the “risk/reward” relationship. What was different about 2022 was that the negative market returns were not only attributable to stocks, but also bonds.

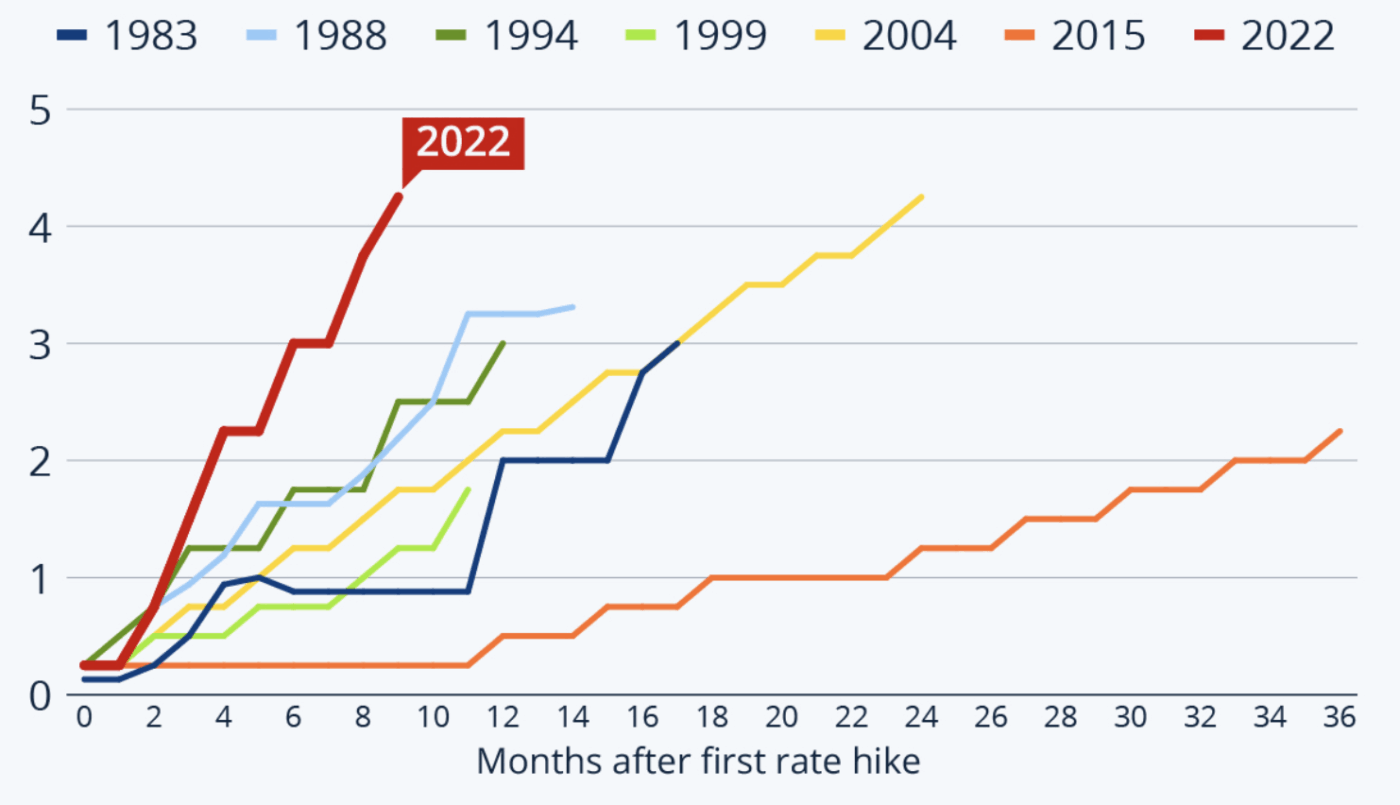

The chart below compares the pace of this current Fed Funds rate hike cycle, compared to historical rate increases. This rapid increase in interest rates caused bond portfolios to experience significant declines. With core bond indexes, such as Bloomberg’s Aggregate Bond Index, having a total return of -12.09%, even the most conservative investors were left with very few places to hide.

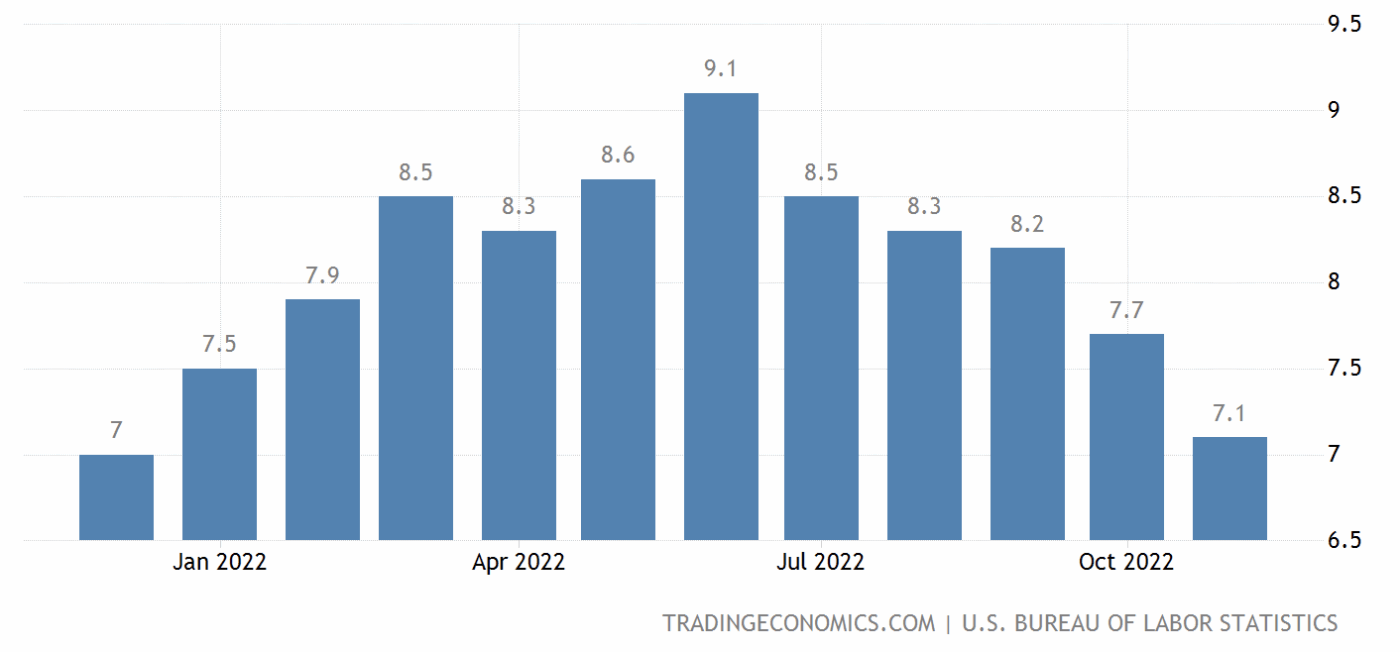

The question on many investors minds was “Why?” Why did Federal Reserve policy makers act so aggressively in raising interest rates? The simple answer is inflation:

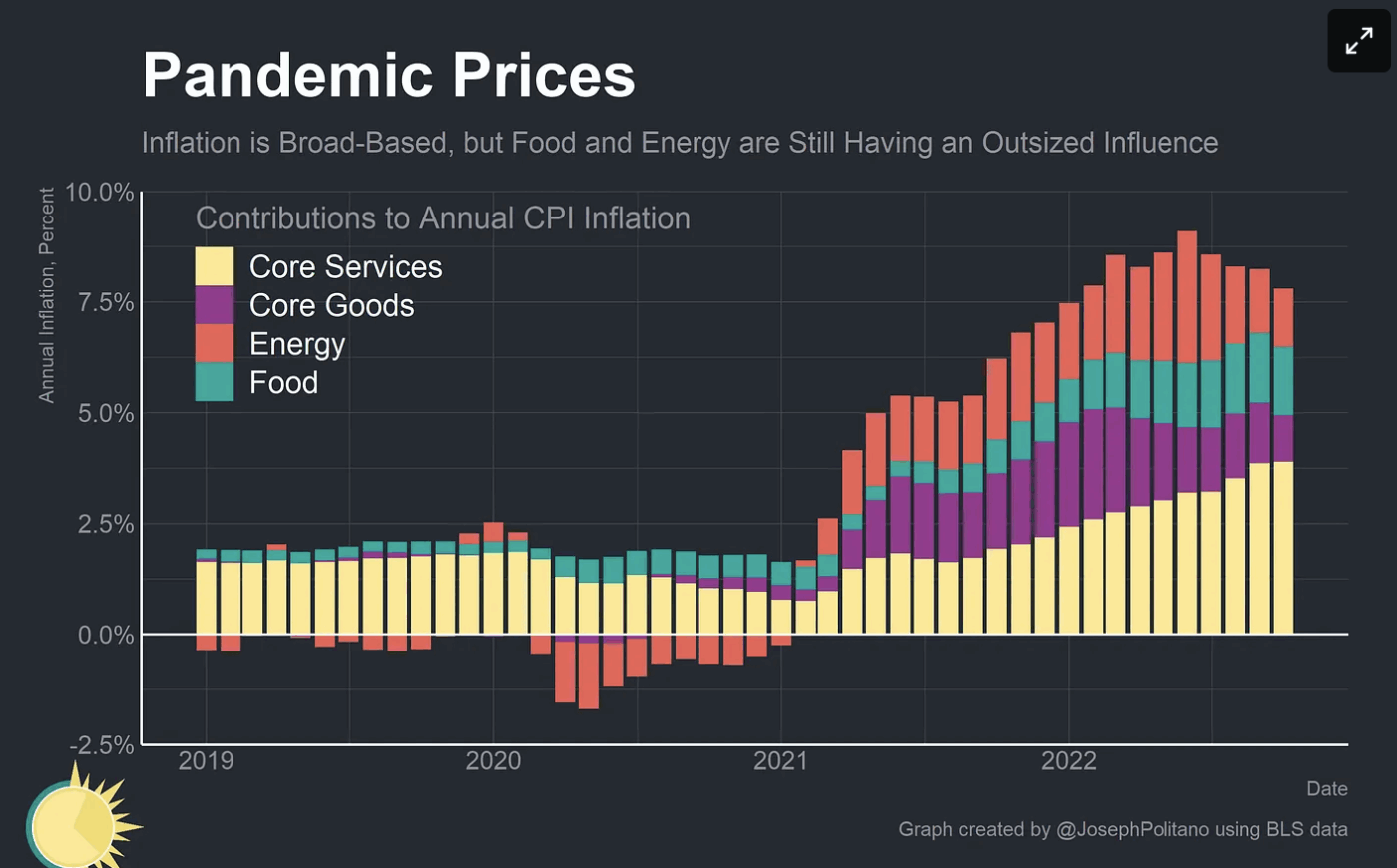

Several factors contributed to the inflationary pressure we experienced in 2022. Most of these factors stemmed from a “once in a 100 year” pandemic resulting in several significant economic effects:

- Supply chain disruptions – the impact of COVID infections and country specific COVID restrictions resulted in a major setback to the global “just in time inventory” supply chain that the world had learned to rely on. The net result was a high demand for a limited supply of goods.

- Energy supply disruptions due to geopolitical events – Russia’s invasion of Ukraine spurred an energy shortage which exacerbated inflation as many global economies shifted away from Russian oil and natural gas supplies.

- Unprecedented fiscal stimulus – in the early days of the pandemic, US congress authorized significant economic stimulus, pumping trillions of dollars into the economy in the form of direct relief, expansion of benefits, increase of government lending and direct grants to states, local governments, schools and universities. This historical stimulus package resulted in more dollars chasing fewer goods, creating higher prices for consumers.

- Labor shortages – as the pandemic stretched on, the impact of worker shortages compounded economic problems. The trucking industry did not have enough drivers, ports did not have enough longshoremen, retailers and restaurants couldn’t keep staff and corporations realized a significant decline in productivity due to losses of employees through pandemic-induced attrition. Fewer workers put pressure on employers to increase wages to attract and retain talent.

If this wasn’t enough, the US and global economy had become accustomed to low interest rates and easy credit that had been in abundant supply since the Great Recession of 2008 and 2009. The compound effect of all these factors together, resulted in inflationary pressure that could have wreaked havoc on the economy in ways we haven’t seen since the late 1970’s, if the Federal Reserve did not act aggressively.

Last year was a good reminder that investing has risk. It is also a reminder that the market is always forward looking. Current stock market prices are rarely a reflection of today’s intrinsic value. Instead, market prices often reflect investors assessment of its future value.

In 2022, as the Federal Reserve worked to hem in inflation, the market realized that the economic growth it had priced into asset prices was not going to materialize. The net result was a corrective sell-off of over-priced assets, based on the new economic realities.

LOOKING AHEAD

Naturally, we’d like to know what is next. Will inflation abate? Will we see loosening monetary policy (lower interest rates)? Will the economy and stock market show positive signs of growth?

The reality is, it is impossible to accurately predict the future, especially when it comes to the stock market. In addition, our own tendency toward recency bias often influences our thoughts about what may happen next. This creates difficulties when managing our own expectations.

We know the market can be reactionary, where the economy is more steady. It’s quite possible what we experienced in the market this year (bear market), is what we may feel in the economy next year (recession). However, we do not know if the market has accurately predicted the severity of a pending recession. It may be that the market will decline further, or even rally back, as more information becomes available.

As for the economy, we know the increased cost of borrowing will be an economic headwind. The continuous threats of layoffs in the tech sector will be unsettling on consumer confidence. The known and unknown geopolitical risks of 2023 and the workout of the global supply chain pressures will continue to create challenges in delivering goods and services.

However, despite our concerns, there are a number of positives that we should remember:

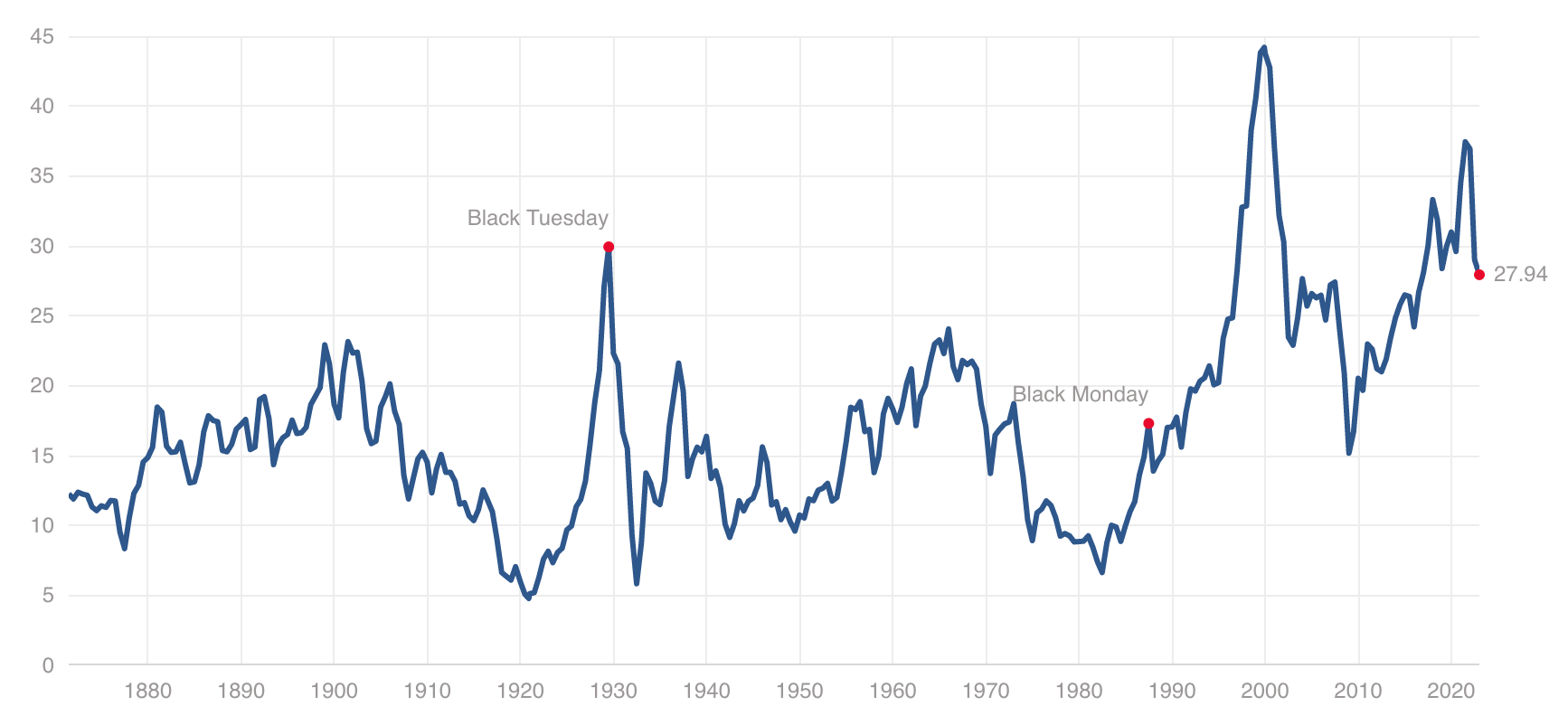

- There has been a healthy reset in stock prices since January 1, 2022, resulting in a 24% discount in the Shiller P/E ratio compared to a year ago. This can be an opportunity to invest in assets at a healthy discount to their prices 12 months earlier.

- The seasonally adjusted unemployment rate is historically low and wages have increased. A low unemployment rate speaks to economic resiliency, while an increase in wages can help with consumer confidence.

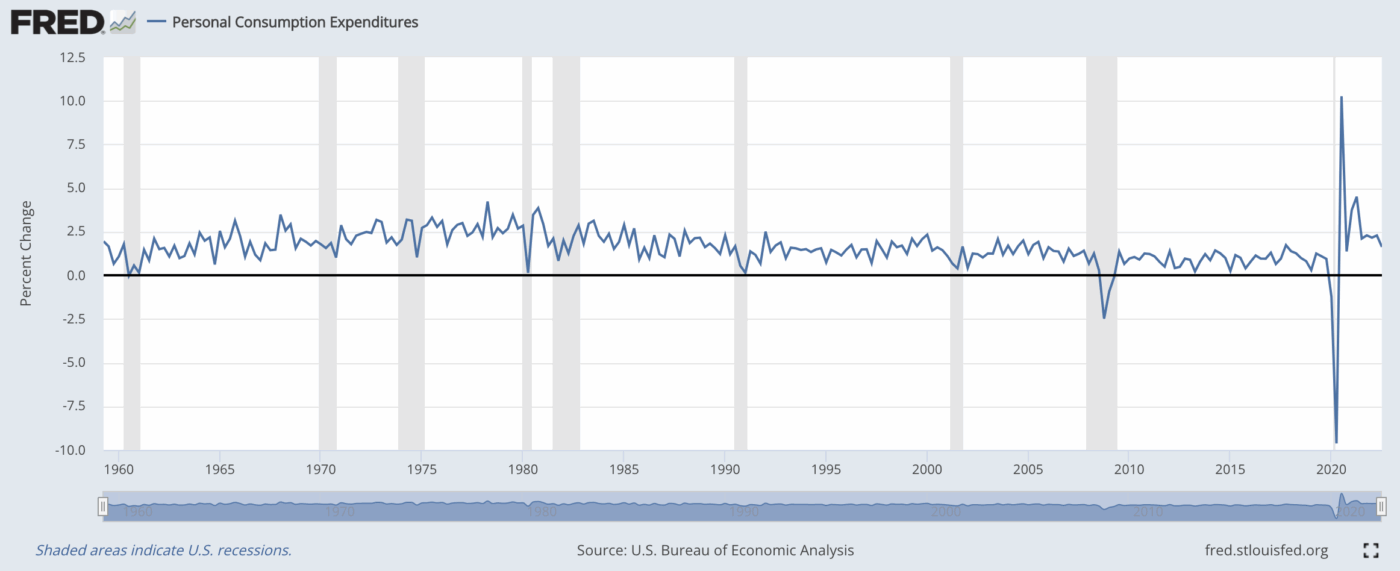

- People are still spending. 70% of the nations GDP is driven by consumer spending, and compared to the height of the pandemic, people are definitely spending more.

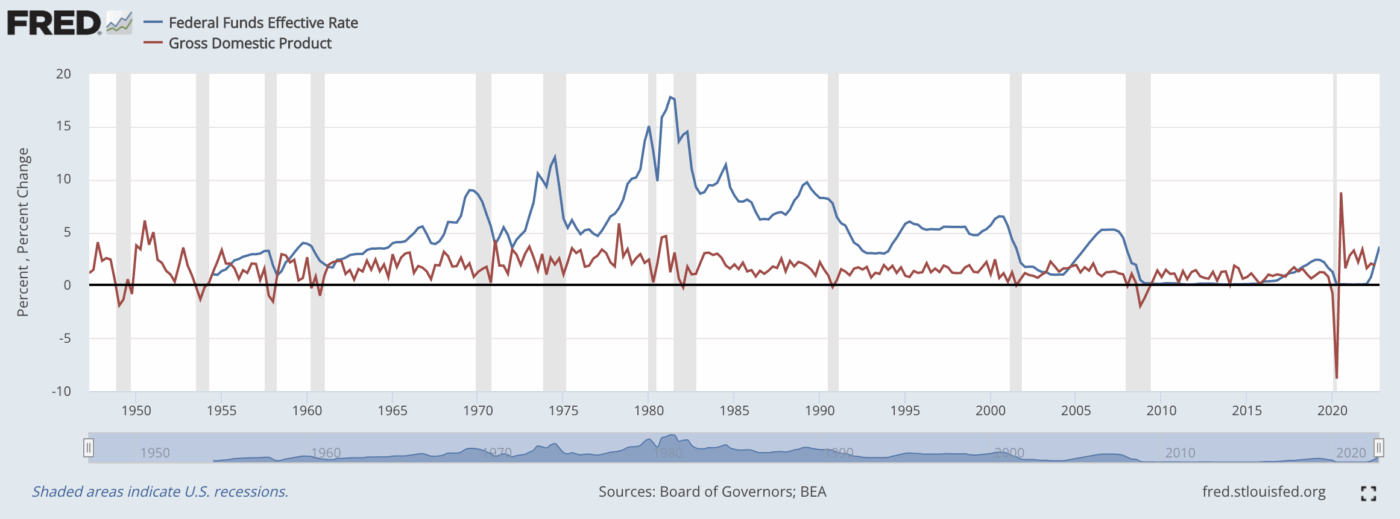

- Economic growth (red line) has been historically resilient through high interest rate environments (blue line), going all the way back to the 1950’s.

MANAGING EXPECTATIONS

While it’s easy to want to focus on the next year. It’s important to remember that investing is a marathon, not a sprint. Since 1928 the market has a total non-inflation adjusted return of 11.63% annually, with 34% of that return coming from dividends and 66% coming from actual price change attributable to earnings growth.

The stock market has proven to be a great way to make our money work for us over the long-term. Volatility will exist, but the persistent investor will be rewarded if they ride it out. Investors who have a well defined investment strategy based on their long-term goals are best positioned to succeed.

Times like this require investors to revisit their financial plan and talk through their portfolio strategy with their investment advisor. This exercise will provide the necessary perspective to stay focused and disciplined during otherwise turbulent times.