The global investment community has been focused on the recent vote by the UK to leave the European Union, broadly referred to as the “Brexit.” This historic event will have economic impacts on the UK and the European Union, as well as their trading partners. Unsurprisingly, equity markets experienced sharp declines in the days following Brexit and have since seen a significant rebound. If you haven’t already, please read our blog post: The Brexit and What it Means.

How Do We Take Advantage of the Brexit?

The volatility and subsequent recovery of the investment markets has been occupying the headlines. As we mentioned in our reblog post, the best decision for most investors during this time is to stay the course. If you’ve done a long-term plan and defined a long-term asset allocation, events like these will come and go with minimal impact on your long-term objectives.

While we may not be making dramatic portfolio changes during these times, there are ways to respond to these types of events. Rebalancing is one key method with which we can take advantage of extreme market movement. In addition, if you have a larger-than-normal cash balance in your savings account, putting some of those funds to work after a market sell-off can be a prudent strategy. Another long-term proven method, is to use dollar cost averaging (DCA).

What is Dollar Cost Averaging (DCA)?

DCA is a systematic deposit program where an investor invests a set dollar amount on a regular schedule regardless of market prices. Depositing $1,000 on the 1st of each month and investing in your core portfolio, is an example of dollar cost averaging. DCA eliminates subjectivity while building your long-term savings. By doing so, investors are less affected by the emotions of fear or greed.

When the markets sell-off, many investors are skittish about putting money to work. However, this is precisely the time individuals should consider investing additional funds. DCA enforces the notion of “buying low.” Conversely, when markets are on the upswing, it can be tempting to buy more of what has been performing the best. However, if you are disciplined in putting the funds to work every month into a diversified target portfolio, DCA can ensure you are not over allocating to “what is hot.”

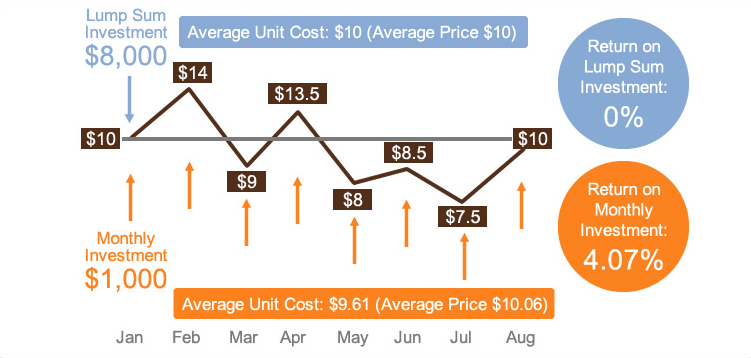

DCA helps eliminate the decision of when to buy into the market, aka “timing the market.” The chart below provides a simple look at how DCA can work when the market experiences volatility:

Source: www.wealthacadamyglobal.com

Many investors already use DCA in their 401(k) or other retirement accounts without realizing it. For many, every time they receive a paycheck, a % of their funds are invested in a 401(k), regardless of what the market is doing. This is dollar cost averaging at work.

It is important we save, save regularly, and invest in a well-built portfolio without bias to market fluctuations. Dollar cost averaging is a proven method to help us meet our long-term goals by eliminating the emotions that often distract us from working towards those goals.