The United States of America always pays its debts. Since the Revolutionary War, the U.S. government has been borrowing money to fund its operations, and it has never failed to make good on its obligations. According to the award-winning financial history, This Time Is Different, no other major power can make that claim.

The founding father of this legacy is Alexander Hamilton, who as Secretary of the Treasury argued persuasively that the full payment of debt was an essential element of the fledging government’s credibility and ultimate independence. In the two and a half centuries since Hamilton set the course, the U.S. government has become the benchmark lender for the entire world. For myriad reasons, but in part because of its historical commitment to paying its debts, no entity on earth can borrow as much money at as low a cost as the United States.

Access to debt financing has been essential to the emergence of the U.S. as the preeminent world power. During World War II, the U.S. issued over $200 billion in debt to outfit its own 16 million men under arms and to substantially finance the British and Soviet militaries. The Great Society programs of the 1960s, President Reagan’s military buildup during the Cold War, and the government interventions under Presidents Bush and Obama to stave off the Great Recession would not have been possible without the ability to raise debt.

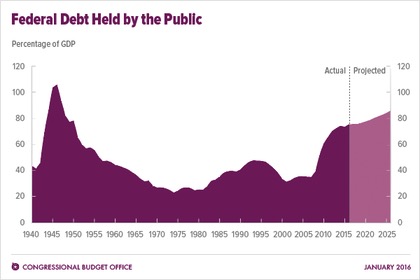

All of that borrowing, however, has added up. Today, the country’s “public debt” (which excludes debt held by the United States government itself) stands at $14 trillion. Adding in the debt owned by government and government agencies (Intragovernmental Holdings), the countries debt is closer to $20 trillion. And each year the government adds hundreds of billions more because each year the government spends more than it takes in through taxes. Even at the low interest rates commanded by the U.S., the annual interest on public debt is around $250 billion. The debt and its associated interest obligations have gone up dramatically over the past fifteen years, largely due to the Iraq war, the government’s response to the Great Recession, and rising health care costs (which increase the cost of Medicare and Medicaid).

Those are huge numbers, but their sheer size can be misleading. The $250 billion in interest the government pays every year is less than 10% of the government’s annual tax revenue, which stands at over $3 trillion. And our $14 trillion “public” debt is approximately 75% of Gross Domestic Product—a ratio that compares favorably to that of Japan (243%), France (98%), the United Kingdom (80%), and Germany (70%). Although many factors play into a country’s capital structure, countries carry large debt loads in part because they can. Debt financing is money not taken in taxes, after all.

It also bears mentioning that while the United States government carries considerable debt, it is also in possession of vast assets, far in excess of its debts. Our federal government is firmly in the black. Measuring the value of the U.S. government’s assets is no simple matter, and of course, much of those assets are not at all liquid—it is small comfort that Zillow estimates the value of the White House at $397 million, since merely putting it up for sale would be an admission of grave national weakness. Nor is the government likely to sell off one of its $10 billion aircraft carriers. But the government does hold a number of large and more liquid assets, such $300 billion in gold and nearly $1 trillion in student loan debts. Oil and mineral reserves on public lands are worth many trillions of dollars—an energy trade group, the Institute for Energy Research, puts the value at $128 trillion.

The most important asset held by the United States government, however, is the right to tax the world’s largest economy, an asset which generates over $3 trillion per year. The U.S. is not in any real danger of being unable to cover its debts for the foreseeable future, even as we continue to pile it up. Spending 10% of the government’s income on debt service is a drag on the economy and less than ideal, but it is not the impending doom so often suggested by pundits and politicians.

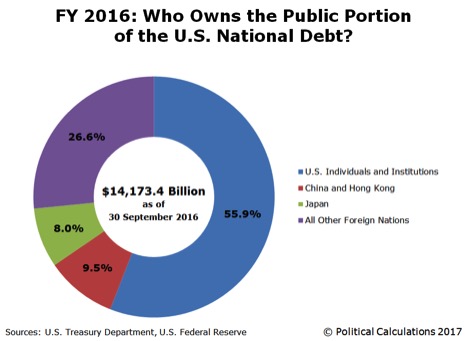

Another concern with this large debt is who holds it. Currently, China and Japan each hold around $1 trillion in U.S. debt (out of a total of $14 trillion public debt), and are by far the largest off-shore holders. Debt opponents sometimes suggest that this gives these countries undue leverage over the United States government. Certainly if you owed someone $1 trillion, or even a mere couple of million, you would probably be very careful not to upset your creditor. But sovereign debt differs from personal loans or other forms of private debt in important ways.

Sovereign debt is integrally tied to the value of a country’s currency. And currency value is of extraordinary importance to countries with large trade balances. China and Japan, whose economies depend on the export of manufactured goods to the United States, buy U.S. debt not because they want to influence U.S. government policy, but in part because they want to influence the value of the U.S. dollar. As exporters, they want to keep the dollar high against their own currencies, since we use dollars to buy all those iPhones and Toyotas.

Moreover, U.S. debt is not an open-ended obligation to pay, such that a debt holder can call in the debt at any time. Rather, it is in the form of securities with specified maturity dates. These are known as Treasury bills, with maturities of one year or less, Treasury notes, with one to ten year maturities, and Treasury bonds, with maturities of twenty and thirty years. The holder of a security receives the face value on the maturity date, and notes and bonds include a fixed interest payment every six months. The only way a debt holder, such as China, can obtain any payment beyond those fixed obligations is to sell securities in the market. And if China or Japan were to radically sell off their U.S. debt holdings, they risk a short term loss selling into declining market, and long term economic harm from a weakening dollar.

Nonetheless, $250 billion in annual interest payments, and a $20 trillion dollar debt (increasing at $700 billion per year) is a matter of genuine concern. The interest payments are a drag on economic growth, and the current rate of growth in the debt itself is likely unsustainable. And so calls to decrease the debt, and to reign in the deficits that create it, are heard from all sides.

The only way to reduce the national debt and associated interested payments is for the federal government to stop running annual budget deficits. That will be no easy task, considering the long term obligations established by Social Security, Medicare, and Medicaid, which account for a significant portion of government’s annual expenditures. Indeed, while it has gotten little attention in the popular media, discretionary spending (spending outside those long term obligations) actually decreased each year from 2010 to 2016. Yet the national debt remains at an all time high. Spending reductions are part of the equation, but the government also needs to raise more money through taxes—ideally through economic growth, which naturally generates more tax revenue, but potentially through higher tax rates or reduced deductions. Inflation can ease the pain by reducing the real value of the debt, but we can’t inflate our way out of debt. Hard choices and coalition building by Congress is required. Unfortunately, recent Congresses have not demonstrated those skills in abundance.

Into this difficult situation enters a peculiar concept known as the debt ceiling. The debt ceiling is a limit imposed by Congress on the federal government’s authority to issue debt. It sets, in actual dollars, a maximum value of the government’s total outstanding debt. Once the total outstanding debt reaches that figure, the Treasury cannot raise any more money by issuing additional debt. And since the federal government spends more than it takes in, once the Treasury can no longer raise money by issuing debt, the government can no longer pay its bills. This means not just debt payments, but federal salary payments, Medicare reimbursement, federal contractor payments, etc. In short order, something would happen that has never happened in the two hundred and fifty year history of the United States—the nation would be unable to pay its debts. Not for a lack of economic ability, but because the government chose to default.

In the past several decades, Congress has shown an increasing propensity to play chicken with the debt ceiling. Various factions have refused to raise it unless given concessions, or even threatened to keep it in place as blunt force means of stopping the growth of the national debt. This summer, President Trump made a much publicized alliance with Democratic leaders in Congress to suspend the debt ceiling (effectively raising it) until December 8 as part of a hurricane relief package. Thus, Congress must act again by December 8 or the U.S. will be unable to pay its debts.

Since it has never happened, the precise impact is unknown, but failure to raise the debt ceiling by December 8 would undoubtedly have substantial negative effects on the United States, and quite likely the world economy. Beyond angry federal employees, contracted parties, and debt holders, there would be a dramatic rise in interest rates. Not just interest rates on U.S. government debt, but interest rates across the board, both because U.S. federal securities are used to set a host of other interest rates, and because the sudden refusal of the U.S. to pay its debts would unleash uncertainty in the world financial markets.

There would also be practical problems and possibly widespread confusion over what obligations would and would not get satisfied. The Treasury handles many thousands of transactions a day, taking and disbursing hundreds of millions of dollars across the federal government’s vast operations. When Congress flirted with refusing to raise the debt ceiling in 2011, the Treasury is rumored to have developed a plan to “prioritize” debt payments over obligations such as government salaries and contractor payments—and effort to maintain the nation’s perfect record on debt payment for a few more days or weeks—but the legality, practicality, and even existence of this plan is unclear. The extensive computer systems, network of trained professionals, and long established customs and practices of the markets in which it operates have been developed on the assumption that the United States, as it has done for every day of its history, will pay all outstanding obligations.

There is no precedent for how the Treasury would discriminate between its obligations and make selective payments in the face of a limit on funds. Not to mention the massively important question of who gets paid, and who gets stiffed. Every choice the government makes will be contested between the President and Congress, and then became the subject of an inevitable wave of lawsuits.

The long term effects are harder to predict, but there is no good news there. Barring the Treasury from issuing additional new debt would do nothing to reduce the existing debt, but it would make servicing that debt far more expensive, due to higher interest rates. The Treasury retires (pays off) debt all the time (as previously issued securities mature), and would continue to retire some debt even in a cash crunch. As the total outstanding debt dropped below the ceiling, the Treasury would issue new debt, until it hit the ceiling again, in order to raise desperately needed cash. But it would have to pay much higher rates on that new debt.

Those higher cost would linger well beyond the immediate resolution of the debt ceiling crisis, as the U.S. would no longer be an entity that always paid its debts. Worse, it would become a nation that had the ability to pay—indeed, the wealthiest nation in human history—but chose not to. That bell cannot be unrung. Anyone doing business with the United States—not just buyers of securities, but contractors, employees, service organizations, etc. would see payments of money owed them not as a foregone conclusion, but as something subject to political whim.

In short, we would have squandered the two hundred and fifty year legacy of prudent management bequeathed us by Alexander Hamilton. It is a fair and reasonable position to ask that the United States reign in the growth of its national debt. But the way to do this is through the regular budget process, tax reform, entitlement reform, and sensible economic and regulatory policy. The debt ceiling, and by extension the credit worthiness of the United States government, should never be used as a political bargaining chip.