Good financial advice boils down to a few simple principles: spend less than you make, maintain a healthy savings rate, invest prudently, manage risk, avoid unnecessary debt, and do your best to plan ahead. Follow these rules of thumb, and chances are, you’ll be in good shape.

Sounds straightforward, right? But here’s the thing, what’s simple isn’t always easy. It’s like saying ‘eat healthy and exercise more, you’ll live longer.’ It’s true… but being consistent day in and day out is tough.

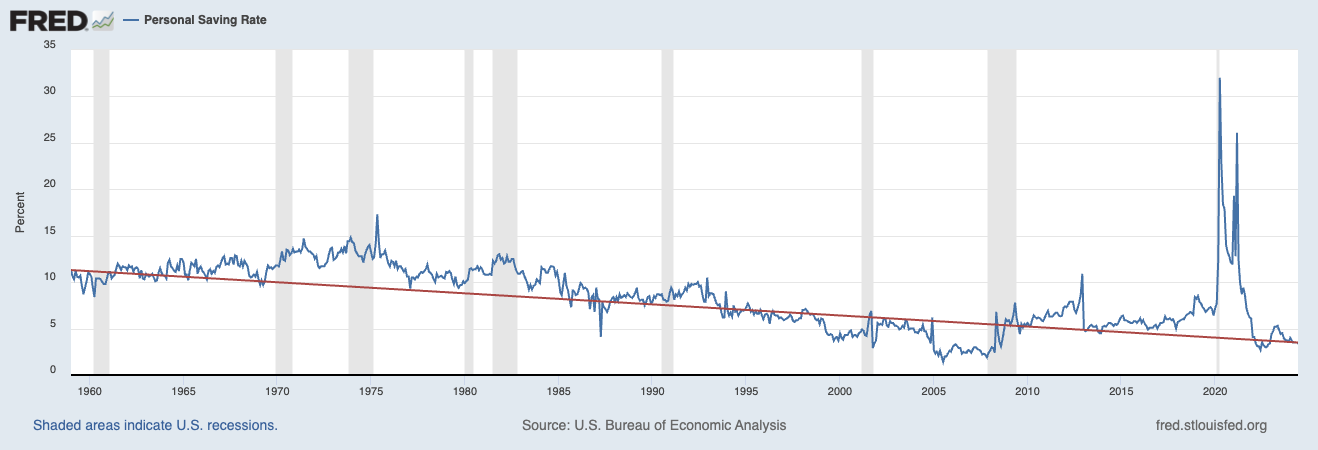

How Much Do Americans Actually Save?

A common rule of thumb is to try to save at least 20% of your income. However, when we look at our country’s personal savings rates, we’re nowhere close to that goal. As of June 2024, the personal savings rate was just 3.4%. Meaning, after taxes and personal spending, only 3.4% of Americans’ incomes were saved. In fact, the only time personal savings rates were above 20% was in the midst of the covid pandemic (not much explaining needed there).

The table below shows the U.S. personal savings rate going back to the 1950s and it’s clear that personal savings rate has been on a downward trajectory ever since.

Arguably, it’s never been harder to save money – high inflation, elevated interest rates, expensive housing, student loans, and the ease of which we can spend money with the advances of technology make it really difficult to save.

While the recommended advice of saving 20% of your income is simple, it’s anything but easy. Building your savings starts with developing healthy habits and making a conscious effort to make it a priority. Here are two links to posts that feature some of my favorite tips and tricks when it comes to building your savings habits: Automate Your Savings & My Favorite 80/20 Relationships

Planning Ahead – The Power of Financial Planning

Life is unpredictable. Our needs, priorities, and desires will change over time. To navigate the unknown, you need to take stock of where you are today, envision where you want to be tomorrow, and ensure you’re on the right track to get there. That’s the power of financial planning.

A solid plan isn’t just about numbers on a spreadsheet—it’s about clarity, conviction, and purpose. When you know exactly what your savings are working towards, you’re not just saving; you’re investing in your future life.

A good advisor doesn’t just work with you to manage your investments—they guide you through pivotal life decisions, keep you anchored to your goals, and help you stay focused on what you can control.

It’s good to plan ahead – simple, right? Taking action? It doesn’t always happen.

Investing is Hard – But It Doesn’t Have to Be

Diversify your portfolio… buy low, sell high… keep your emotions in check… don’t look at your accounts… bear markets are an opportunity… be greedy when others are fearful… you get the point. These nuggets of stock market wisdom make investing seem simple. But, the reality of watching your investment accounts plunge in value during a market sell-off can test even the most disciplined investor.

Investing prudently is about crafting an investment and savings strategy that is aligned with your goals. Developing a strategy that you can have conviction in during bull markets and the inevitable downturns is paramount.

Here are a few of my favorite charts that show why investing is hard (and easy).

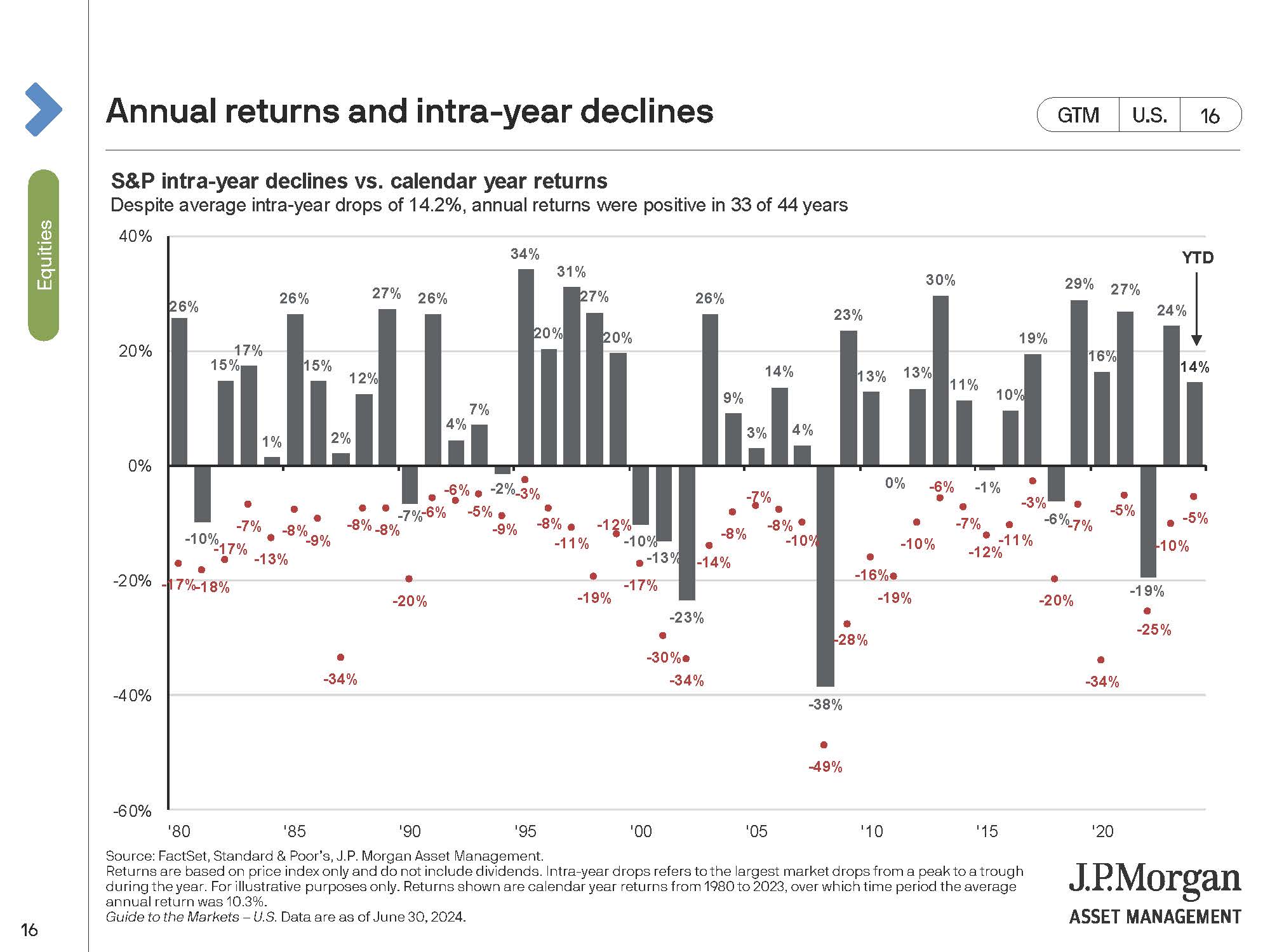

S&P 500 Intra-Year Declines vs Calendar Year Returns

- Why it’s hard: look no further than 2000 – 2003, 2008, & 2022 in the chart above to see significant market drawdowns. In addition, even positive years will have their own gut wrenching downturns – the average intra-year price drop in the S&P 500 is -14.2% (red dots).

- Why it’s easy: S&P 500 returns were positive in 33 out of 44 of those years going back to 1980.

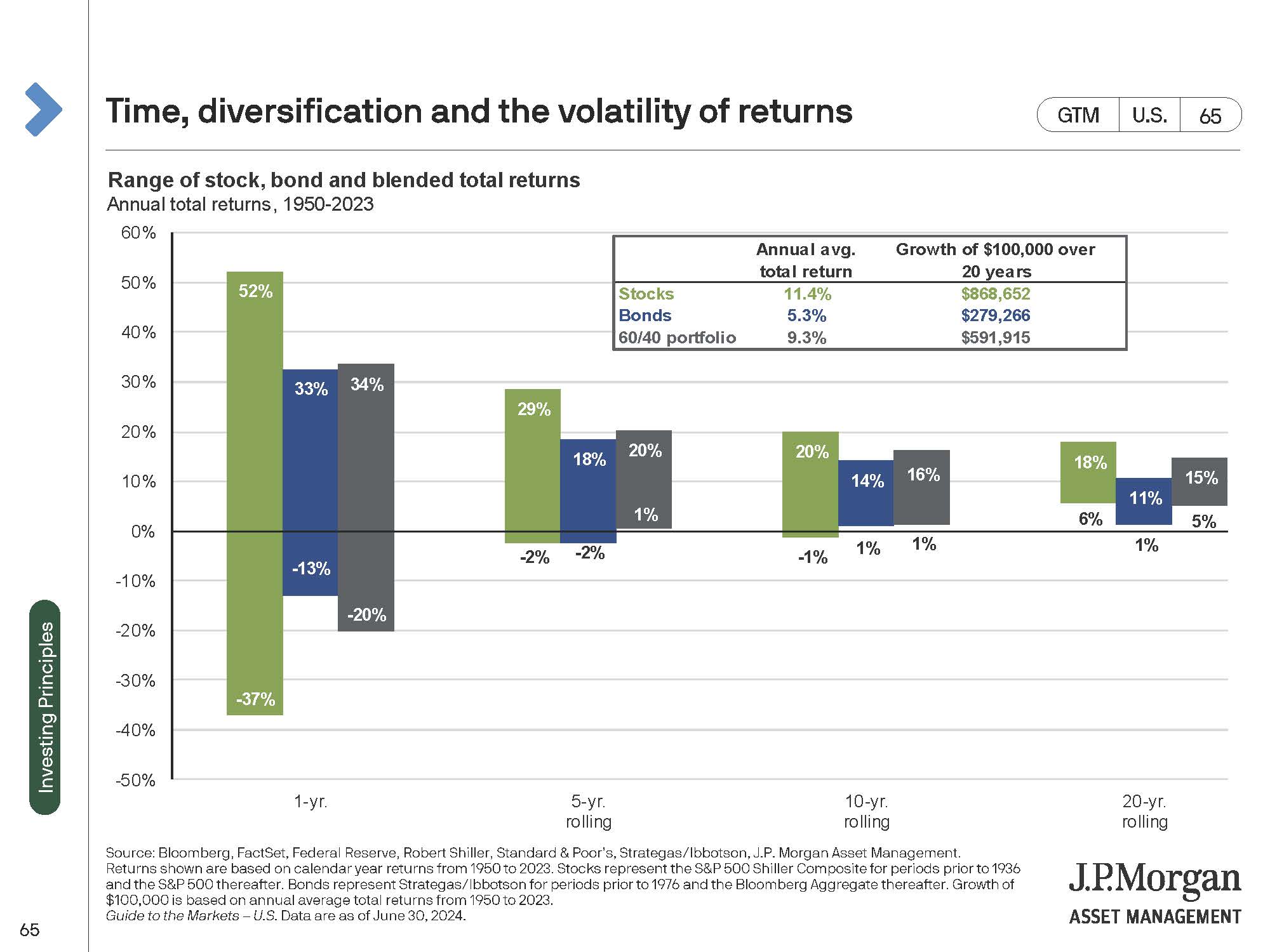

The Range of Stock, Bond and Blended Returns

- Why it’s hard: in any given year, your investments can plummet in value.

- Why it’s easy: when time is on your side, your range of potential outcomes is clearer.

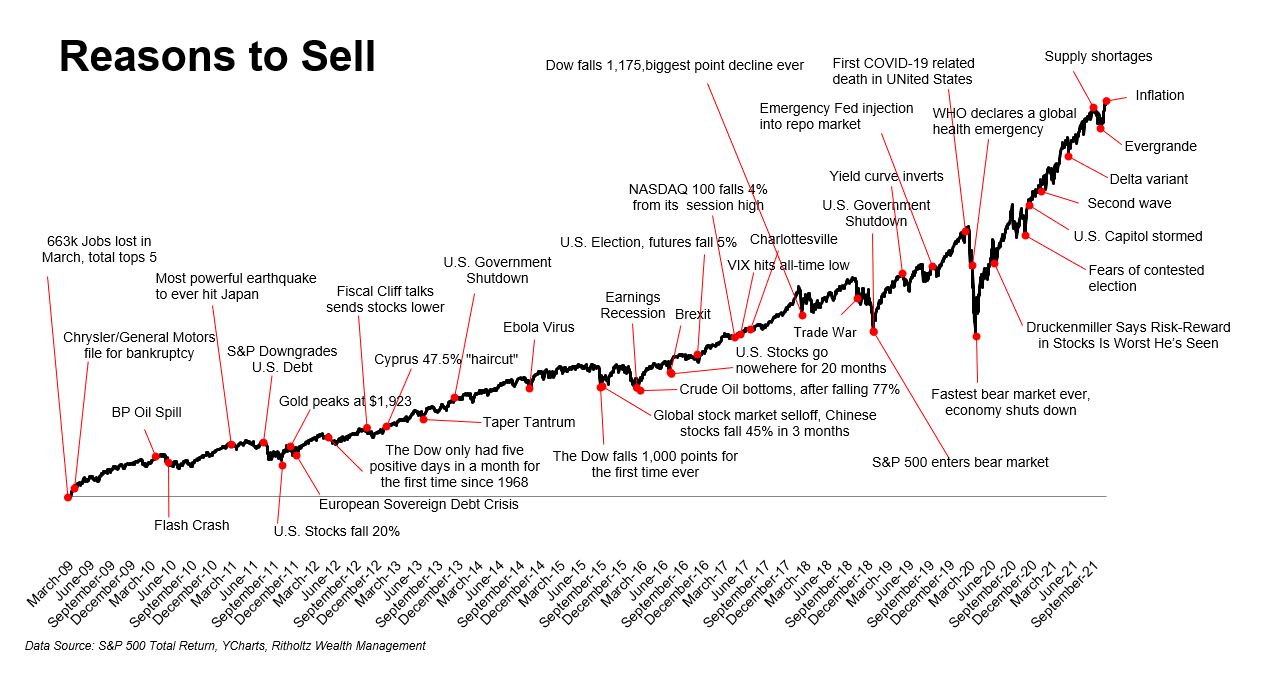

There’s Always a Reason to Sell

- Why it’s hard: zoom in on any major event. Try to go back to that moment – fear took over.

- Why it’s easy: there’s always going to be something… zoom out and you’ll notice that the line is still going up and to the right.

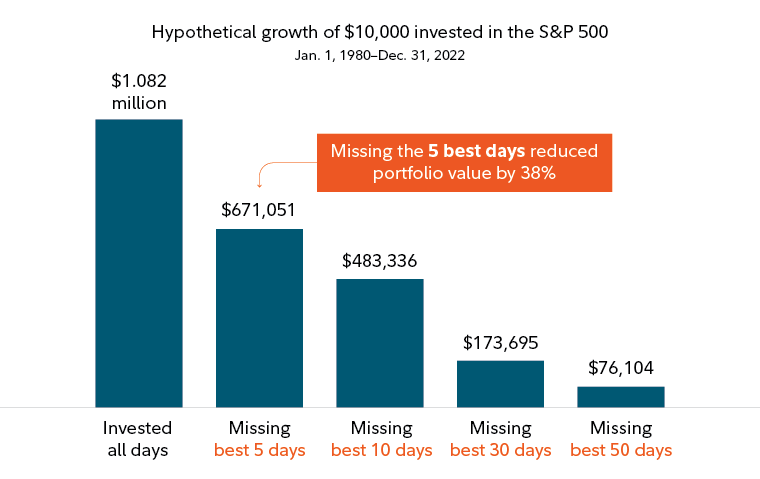

Missing the Best Days in the Market

- Why it’s hard: if you only missed the 5 best days to be invested, you missed out on $411k.

- Why it’s easy: stay invested. Trying to time the market is a fool’s errand.

Is all the above simple sounding? Sure. Easy to do? Not quite. But with the right plan and team behind you, you’ll be in a better position because of it.