How do you solve a problem like commodities? Sound of Music, anyone? Well, if you are not a fan of musicals, that is okay. Chances are at this point in the market cycle, you are probably not a fan of commodities, either. Commodity prices are clearly a hot-topic right now and not in a good way. As anyone who owns commodities knows, returns for the asset class have been more than frustrating the last several years.

What Is Happening?

Commodities prices and more specifically commodities futures returns have suffered as of late due to a combination of global events. A primary driver of poor commodities returns has been the drop in the cost of oil. North America’s oil boom, and OPEC’s decision to not cut its own production quotients, has resulted in a supply glut. This excess supply of oil has driven the price per barrel of WTI crude down to levels not seen in over a decade.

In addition to the excess supply of oil, we have seen weakening economic growth in large economies such as China. China’s position as the second largest economy in the world has a significant impact on global prices. If economic growth in China, or other rapidly developing economies such as India or Latin America, begin to slow down, then a reduction in demand for commodities is sure to follow. When you combine the drop in oil prices with a slow-down in global consumption, the net result is a significant downside pressure on commodities returns.

What Are Commodities?

Commodities are much more than just energy. In fact, commodities include agriculture products (wheat, soy, corn, etc.), metals (lead, aluminum, copper, etc.) as well as beef, pork bellies and other raw goods that go into the manufacturing process. However, more often then not, energy prices account for 50% of the cost to produce other commodities. This means that as these costs drop, it is more cost effective to mine more metals or produce more corn, resulting in an increase of supply of these other commodities.

Commodities as an investment involves the use of commodities futures contracts, either owned directly, through pooled investment vehicles, or indexes that track commodities future prices. Typically, only producers and/or distributors of commodities will actually physically own, store and transport commodities. Most other investors use futures to gain exposure in some form.

Should I Buy or Sell?

The real question on many investor’s minds is why they should own commodities at all? With returns being negative the last several years, what is the benefit? The purpose of this post is to highlight the primary reason to include commodities as an asset class in a diverse long-term investment portfolio.

The distinct benefits of holding commodities in a long-term portfolio are as follows:

1. Commodity prices historically have been correlated with inflation

2. Historically, commodity returns have low correlations with the returns of stocks and bonds

3. The risk return profile of commodities futures contracts over the years, with the exception of the last 10 years, has been similar to that of US equities.

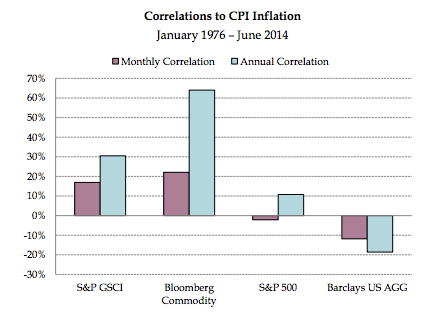

Lets address each one. First, lets review the correlation between commodities and inflation. Below is a chart highlighting the correlation between two key commodity indexes (S&P GSCI and Bloomberg Commodity Index) and inflation. You can see that both indexes have higher monthly and annual correlations to CPI inflation than either the S&P 500 or Barclays US Agg bond index. The period being measured in this case was from 1976 to 2014 (38 years):

* Source Meketa Investment Group 2015

It is well-documented that commodities provide a good hedge against inflation. It makes sense, as you consider commodities are the earliest inputs into the manufacturing of all the goods we consume. As these early inputs rise in price, the cost of all goods manufactured downstream also increase.

Next, lets consider the diversification benefits commodities generally provide to a long-term portfolio. Diversification is achieved in a portfolio when assets in the portfolio have correlations closer to zero than they do 1 or -1. A correlation of 1 between assets in a portfolio, means their returns and price movements move in lock-step with one another, moving in the same direction. A correlation of -1 means their price movements are moving in opposite directions. True diversification comes when correlations are closer to zero. As the world’s capital markets become more integrated, achieving a correlation of zero is like finding the Holy Grail. However, working on keeping correlations in a portfolio lower is what a portfolio manager should continuously strive for over time.

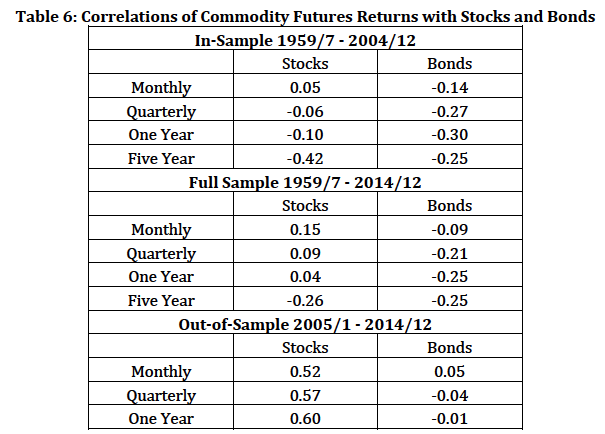

Below, is a table of correlations between commodity futures contracts with stocks and bonds. It highlights correlations for the distinct periods of 1959-2004, 1959-2014 and 2005-2014.

{kind=link}

*Source: Yale ICF Working Paper No. 15-18, “Facts and Fantasies about Commodity Futures Ten Years Later

In the first section of the table, for the period 1959-2004, correlations between commodities and stocks/bonds were near zero, if not slightly negative. In the last part of the table, the most recent period of 2005-2014, correlations between commodities and stocks went up (this increase in correlation between asset classes is true of many asset classes during times of significant market volatility, such as we experienced during the Great Recession). However, correlations with bonds still remained near zero. When the two periods are combined, 1959-2014, the long-term averages still remain close to zero.

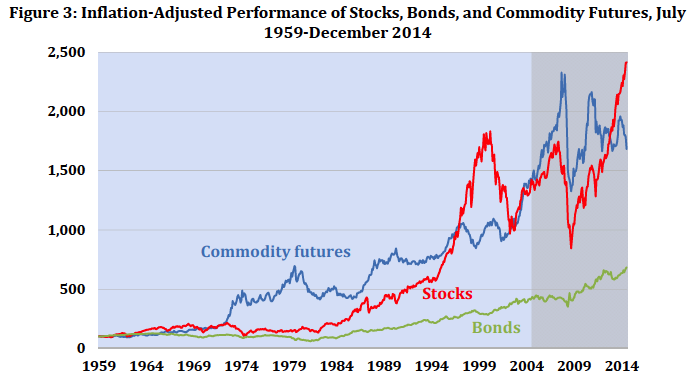

It’s clear that including commodities in a portfolio provides an inflation hedge and diversification benefits. But what about long-term returns? The same paper highlighted the inflation-adjusted performance of stocks, bonds and an equal-weighted commodity futures basket from 1959 to 2014 in the graph below. While the last 10 years clearly show a sideways movement in commodities futures, you can see the price appreciation over the longer time-period is not dissimilar to stocks and much better than bonds.

*Source: Yale ICF Working Paper No. 15-18, “Facts and Fantasies about Commodity Futures Ten Years Later

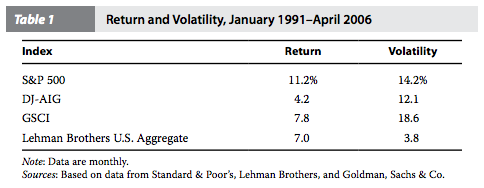

However, more recently, you can see that the returns of commodities have come down compared to stocks. The table below shows what the GSCI index and the DJ-AIG (now the Bloomberg Commodity Index) returned for the period between 1991 and 2006. While the returns are below the returns of stocks (S&P 500) and bonds (Lehman Brothers US Aggregate) represented in the table, they are none-the-less significantly positive. And while the recent returns have been negative and the nearer-term trend has also been negative, the potential for positive long-term returns of commodities is sufficient enough to warrant a place in a portfolio.

*Source: CFA Institute

When Will Commodity Returns Recover?

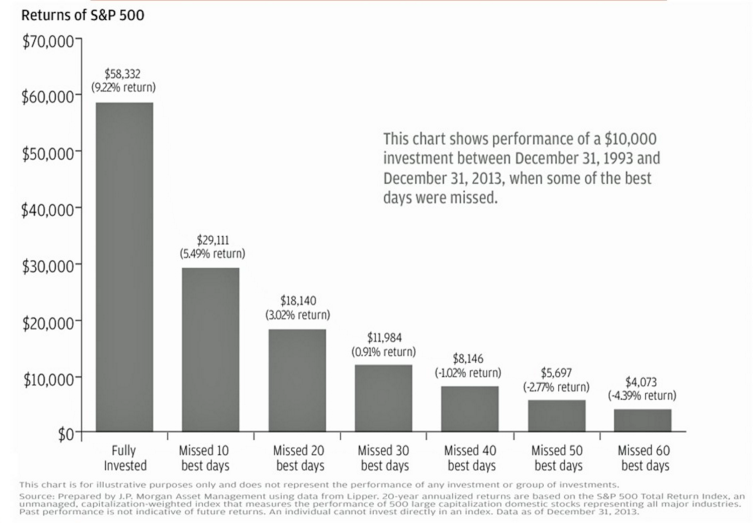

When it comes to asset class returns in general, a VERY important point needs to be considered: most of the long-term returns of any asset class are concentrated in brief periods of time. Below is a chart highlighting the effects of missing a handful of the best days of returns for the S&P 500 between 1993 and 2013. The result of missing just the best 10 days was a 40% drop in long-term returns. If you missed the 20 best days of that period, your returns were cut by more than 60%. The chart below highlights the affects of missing those days on a portfolio of $10k.

*Source: Business Insider, JP Morgan

The point is that attempting to time when to be in or out of commodities is no different than timing when to be in or out of equities. If you miss a small number of days over the long-term, you could quite easily miss out on the majority of the returns. This is why maintaining exposure and rebalancing in light of market events is the best approach to owning this asset class, as is true for most asset classes.

So, while you may be wary of recent commodities returns, there are many reasons to own them as part of a broader investment strategy. Investors interested in hedging inflation, increasing diversification and adding an asset class with positive long-term return premiums over inflation, may benefit from maintaining or adding the asset class to their portfolio.