Our clients often ask us about real estate, and what we think about buying or selling a primary residence, a vacation home, or an investment property. This is hardly surprising—for many of our clients, their family home is by far their largest asset. What’s more, most of our clients live in either the Seattle or San Francisco areas, both of which have experienced extraordinary real estate appreciation in recent years.

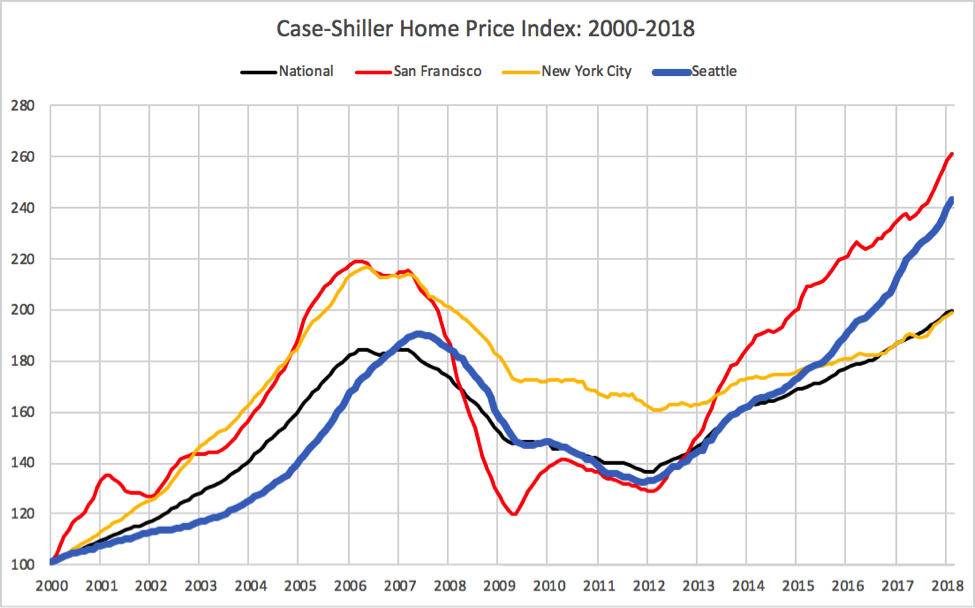

Seattle home prices in particular are appreciating far more quickly than the national average, and are catching up with real estate hyper-growth poster-child, San Francisco:

As much as homeowners might welcome this sharp increase, however, memories of the housing collapse of 2007-2008 have kept a question front and center for many of us: are we in a real estate bubble, and if so, when it is going to pop?

The short answer is simple: we don’t know. Neither does anyone else. Sure, the financial media is full of pundits who claim to know, but if they really knew the future of real estate prices, they would not be spilling the beans on CNBC.

The more important answer for our clients, however is this: it doesn’t matter very much. Because for most people, the right real estate investment decision is based on personal circumstances, not the state of the market. Why? Because real estate is unlike any other investment.

First and foremost, real estate is an investment you can use. It has “utility” in economic terms, which is a fancy way of saying you can live in it (or vacation in it, or rent it out for income). And since you need a place to live, this is a very important benefit—because if you don’t own a home, you most likely will have to incur costs renting one. That’s not true of stocks. You can’t live in a hundred shares of Amazon, nor does owning a hundred shares of Amazon save you from renting a hundred shares of Microsoft. And this is not just an economic truth. You don’t come home from a long day at work and sink comfortably into a 10-year Treasury bill, while your kids chase the dog up and down the fixed-income bond ladder out back. Real estate is more than an investment; it’s your home.

Moreover, real estate is the hands-down, all-world champion of long term investments. Land will always be in demand, there is a fixed and limited amount of it, and it cannot be replaced by any technological or cultural innovation. Reversals in real estate values are inevitably followed by greater growth, and even during downturns, you can still live in it. If you bought a home in 2007, at the peak of the market, your home lost nearly half its value over the next two years. But provided you kept your home, you had a place to live and you recouped your paper losses by 2015, and have been back on the investment gain train ever since.

Not only is real estate a reliable long-term investment, it is—thanks to the ready availability of mortgage lending and the associated tax deduction—an extraordinarily efficient one. Consider what you can do with $100,000 in either the stock market or in real estate. If you invest that money in the market, and the market goes up 10%, that’s a nice return, and you’ve made $10,000. But with real estate, that $100,000 can serve as the down payment on a $500,000 property. And if that property goes up by the same 10%, you don’t make just $10,000, you make $50,000. Of course, you have to make mortgage payments along the way, and assume the costs of insurance and maintenance, costs not required for a stock market investment, but those costs provide you a place to live, and a good portion of them—the interest on your loan—are tax deductible.

The utility of real estate, its long-term reliability, and its efficiency all make real estate an excellent investment to hold for long periods, regardless of what the market does year-to-year. Meanwhile, as good a long-term investment as real estate can be, it is a terrible short-term investment, because it has exceptionally high transaction costs. Buying or selling real estate takes a long time, requires a lot of work, and incurs a variety of financial costs, from real estate agent commissions to new furniture. And because rents tend to move roughly in line with real estate values, selling your home into a growth market offers only a limited net return, since you will have to put the proceeds towards rent (and lose the mortgage interest tax deduction).

Because real estate—for most of us—is a long-term investment that puts a roof over our head, but also requires financial and practical participation, personal circumstances matter far more than market conditions. The right time to buy a house is when you need a place to live, when you have the capital for the down payment and moving-related costs, when you are willing to take on the maintenance responsibilities, and when you have confidence your earnings power is sufficient to meet the mortgage payments and other costs. The right time to sell a house is when you no longer need it, or when you no longer can or want to make the mortgage payments.

Consider one common question we get from clients. The clients bought their home in the 1990s for $200,000. Their neighbor’s nearly identical house just sold for $800,000. Surely this is not sustainable—should the clients sell and secure their windfall profits before the inevitable market collapse? Well, the cash would be nice, but then where are these clients going to live? Where are they going to invest that cash? Buy another house for the same price, and all they have done is incur substantial transaction costs without changing their exposure to the market. Buy a less expensive house and now they have a smaller house, or a house in a less desirable neighborhood (there is a reason it is less expensive, after all), plus they still need to find an investment for the cash they secured—are they so sure the housing market is due for a collapse, but the stock market is not?

The bottom line is that for most of us—people without extensive real estate portfolios—the right time to buy and sell real estate is a function of our personal circumstances, not the market. Real estate is the ultimate buy and hold investment, and long-term trends always matter more than short-term market fluctuations.

Nonetheless, we recognize that the real estate market is a hot topic these days, especially in Seattle and San Francisco. And while we do not believe that we or anyone else can reliably predict future price movements, there are indicators, such as household debt, which can suggest when the real estate market is at a lesser or greater risk of a decline. Next month, we will take a look at some of those indicators, and discuss what makes a real estate bubble, and why they pop. You might be surprised by our assessment of current real estate values.